Captive Insurance 101: Everything You Need to Know About Captive Insurance

A Primer on Captive Insurance

What is a captive insurance company?

Definition

A “captive insurance company” is a subsidiary owned by one or more parent organizations established primarily to insure the exposures of its owner(s). The captive assumes a portion of the risks insured, and the balance is assumed by another insurance company known as a “reinsurance” company.

Evolution of Captives

The term “captive” dates back to the early 1950’s when Fred Reiss created Steel Insurance Company of America for his client, Youngstown Sheet and Tube Company in Ohio. Youngstown owned its own mines, which it called “captive mines”, because they were used to mine ore for the company’s mills. Reiss created Steel Insurance Company of America to write insurance solely for those mines, thereby calling it a “captive insurance company”. Reiss was the first person to realize that he could create a profit center from the cost of insurance.

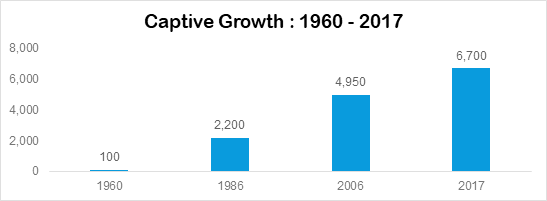

By 1960, there were more than 100 captive insurance companies in the United States, writing insurance for their parent companies. In 1986, there were over 2,200 captives worldwide, which grew to 6,700 by the end of 2018 (Source: CPA Journal, Captive Insurance Companies, 12/19/2018). Figure 1 illustrates how captive growth has accelerated over time due to the many benefits of captives which we will discuss in Section 2.

Figure 1: Captive growth has accelerated over time.

Source: IRMI, www.captive.com, “SRS Charts the Total Number of Active Captives for 2017”, March 2, 2018.

Captive Structures

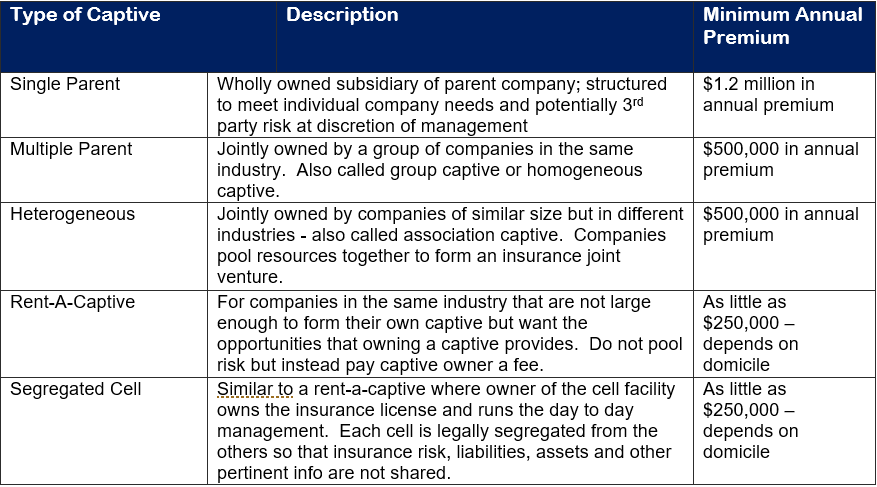

There are five types of captive structures – single parent, multiple parent, heterogeneous, rent-a-captive, and segregated cell. See Table 1 below for descriptions of each structure.

Table 1: Five Types of Captive Structures

Source: www.captives.com, “Five Questions to Ask When Considering Captive Insurance.”

Coverage Types

Captives provide enterprise risk financing for the following types of coverage:

- Employee healthcare insurance

- Workers compensation

- Product liability

- Professional liability

- Extended warranty and service contracts

- Cyber security and terrorism

- Other company-specific risks

When considering a captive, it makes sense to look at your entire commercial risk portfolio in order to determine the optimal captive structure.

Captive Domicile

The “captive domicile” is the state, territory or country where a captive insurance company is located, that also licenses the insurance company and has primary regulatory oversight.

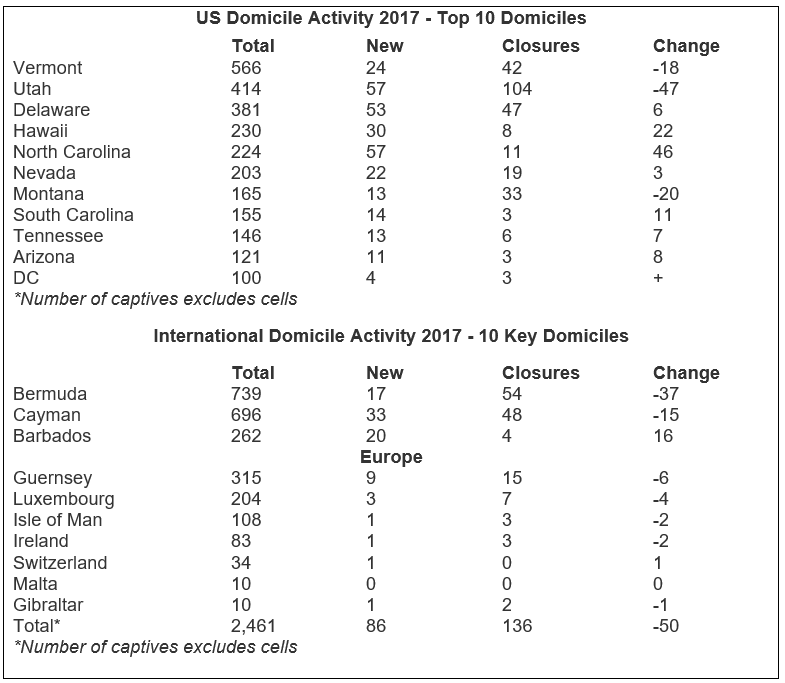

Below is a list of the top domiciles for captives both in the United States and internationally. Bermuda is the top domicile internationally followed by the Cayman Islands as both have favorable regulatory climates, established professional infrastructure (captive management, legal, and accounting firms), and favorable taxation. Vermont is the top domicile in the United States, but other states continue to pass laws to encourage captive creation.

Table 2: U.S. & International Domiciles Summary – 2017

Fronting Company

A “fronting company” is a licensed insurer that issues an insurance policy on behalf of the captive without the intention of transferring any of the risk. The risk of loss is retained by the captive with an indemnity agreement. Fronting arrangements allow captives and self-insurers to comply with financial responsibility laws imposed by many states that require evidence of coverage written by a licensed insurer. The fronting company (insurer) assumes a credit risk since it would be required to honor the obligations imposed by the policy if the captive failed to indemnify it. Fronting companies charge a fee for this service, generally between 5 and 10 percent of the premium being written. (Source: IRMI.com)

How does a captive work?

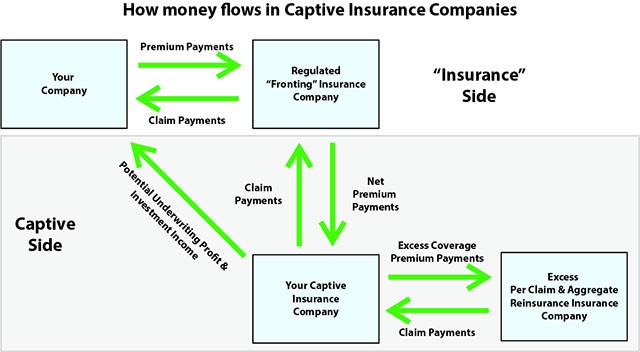

The graphic below illustrates how captive insurance companies work and the flow of money between the parent, the fronting company, the captive, and the reinsurance company. As you can see, the “fronting” company is just a pass through and the captive – like a typical insurance company – uses a reinsurance company to provide excess coverage for unexpected and/or high claim losses.

Figure 2: The Flow of Money in a Captive Insurance Company

Source: http://www.stopbeingfrustrated.com/captive-basics.html

What are the advantages of a captive?

When set up and managed effectively, captives offer significant benefits, including:

- Coverage tailored to meet the parent’s specific needs and risk profile – especially when coverage is unattainable due to availability or price.

- Reduced operating costs

- Insurance coverage purchased in the conventional market reflects a significant markup to pay for the insurer’s acquisition costs, administration, and overhead, as well as profit to the insurer.

- A captive can reduce these costs – with the size of the reductions dependent upon the captive’s loss experience and claims handling costs.

- Revenue recognition of extended warranty (service contract) margin

- Without a captive, companies are forced to earn the entire amount based on a curve or pro-rata. But with a captive, they cede the premium and can take the margin into income.

- Investment income to fund losses

- With premiums paid upfront and losses funded over time, investment income can accumulate in a tax-free domicile, providing additional funds to pay for losses and a corresponding reduction for further captive funding.

- Ability to access reinsurance markets directly

- Because reinsurers deal primarily with insurance companies, a captive allows the parent to go directly to the reinsurer and avoid unnecessary markups.

- Ability to customize insurance programs and greater control over claims

- A captive can finance any risk it chooses, customize the terms of its policies, and specify claims handling and procedures.

- Tax advantages

- Captives offer a number of tax advantages, such as: accumulation of underwriting and investment income in a tax friendly domicile, ability to deduct paid premiums for the insured, and a variety of other tax incentives, depending on the domicile.

Sources: Captive.com, “Captive Insurance – Why or Why Not?”, June 10, 2019; State of Vermont, Department of Financial Regulation, www.dfr.vermont.gov/captives/advantages-captive-insurance

Is a captive right for my business?

Typically, the best candidate for a captive program is a company with high insurance premiums, low claim frequency, steady cash flow and palatable risk. However, there are other reasons (as discussed in the previous section) that a company may consider a captive. A company may also wish to combine its overall enterprise risk across not only its warranty program, but also its employee benefits, healthcare and/or workers compensation.

If you have determined that a captive could be a great option for your company, your next step is to contact a trusted captive expert that can help you conduct the necessary due diligence, determine the right partners, set up the captive structure and even manage the day to day captive operations.

After, Inc. (www.afterinc.com) has been offering Warranty Program Administration – including captive set-up and management – to top tier manufacturing clients for over 15 years. If you are interested in discussing a potential captive for your business, contact us at http://afterinc.com/contact/. We look forward to hearing from you.